Page 53 - 次貸風暴下的省思-解開CDS及CDO密碼

P. 53

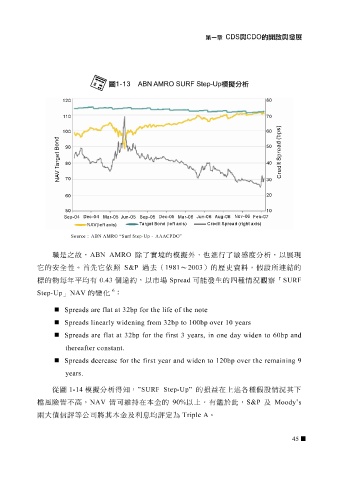

Source : ABN AMRO “Surf Step-Up - AAACPDO”

職是之故, ABN AMRO 除了實 境 的 模 擬 外, 也 進 行了 敏感 度分 析 ,以展現

它的 安全 性。 首先 它 依 照 S&P 過去( 1981 ~ 2003 )的 歷史 資 料 , 假設 所 連 結的

標的 物 每年 平 均有 0.43 個 違 約,以市場 Spread 可能發生的四種 情況 觀 察 「 SURF

6

Step-Up 」 NAV 的 變 化 :

Spreads are flat at 32bp for the life of the note

Spreads linearly widening from 32bp to 100bp over 10 years

Spreads are flat at 32bp for the first 3 years, in one day widen to 60bp and

thereafter constant.

Spreads decrease for the first year and widen to 120bp over the remaining 9

years.

從 圖 1-14 模 擬 分 析 得 知 , ”SURF Step-Up” 的損益在上述 各 種 假設 情況 其 下

檔 風險皆不 高 , NAV 皆可 維 持在本金的 90% 以上。有 鑑 於此, S&P 及 Moody’s

兩大債信評等公司將其本金及利 息 均評定為 Triple A 。

45