Page 54 - NO.153銀行家雜誌

P. 54

तйΆྌ

Special Report

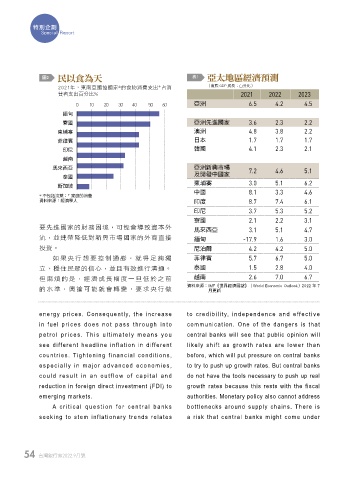

圖2 民以食為天 表1 亞太地區經濟預測

+

2021年,東南亞國協國家*的食物消費支出 占消 (實際 GDP 成長;百分比)

費者支出百分比% 2021 2022 2023

亞洲

0 10 20 30 40 50 60 6.5 4.2 4.5

緬甸

寮國 亞洲先進國家 3.6 2.3 2.2

柬埔寨 澳洲 4.8 3.8 2.2

菲律賓 日本 1.7 1.7 1.7

印尼 韓國 4.1 2.3 2.1

越南

馬來西亞 亞洲新興市場 7.2 4.6 5.1

及開發中國家

泰國

柬埔寨 3.0 5.1 6.2

新加坡

中國 8.1 3.3 4.6

+

* 不包括汶萊; 家庭的消費

資料來源:經濟學人 印度 8.7 7.4 6.1

印尼 3.7 5.3 5.2

寮國 2.1 2.2 3.1

要先進國家的財務困境,可能會導致資本外 馬來西亞 3.1 5.1 4.7

流,並連帶降低對新興市場國家的外商直接 緬甸 -17.9 1.6 3.0

投資。 尼泊爾 4.2 4.2 5.0

如果央行想要控制通膨,就得足夠獨 菲律賓 5.7 6.7 5.0

立、穩住民眾的信心,並且有效進行溝通。 泰國 1.5 2.8 4.0

但麻煩的是,經濟成長幅度一旦低於之前 越南 2.6 7.0 6.7

的水準,輿論可能就會轉變,要求央行做 資料來源: IMF《世界經濟展望》(World Economic Outlook)2022 年 7

月更新

energy prices. Consequently, the increase to credibility, independence and effective

in fuel prices does not pass through into communication. One of the dangers is that

petrol prices. This ultimately means you central banks will see that public opinion will

see different headline inflation in different likely shift as growth rates are lower than

countries. Tightening financial conditions, before, which will put pressure on central banks

especially in major advanced economies, to try to push up growth rates. But central banks

could result in an outflow of capital and do not have the tools necessary to push up real

reduction in foreign direct investment (FDI) to growth rates because this rests with the fiscal

emerging markets. authorities. Monetary policy also cannot address

A c riti cal ques tion for c entral banks bottlenecks around supply chains. There is

seeking to stem inflationary trends relates a risk that central banks might come under

54 台灣銀行家2022.9月號

1 5% JOEE