Page 374 - 國際金融市場實務

P. 374

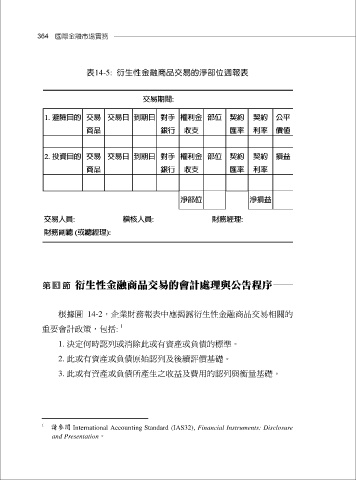

364 國際金融市場實務

表14-5: 衍生性金融商品交易的淨部位週報表

根據圖 14-2,企業財務報表中應揭露衍生性金融商品交易相關的

1

重要會計政策,包括:

1 決定何時認列或消除此或有資產或負債的標準。

2 此或有資產或負債原始認列及後續評價基礎。

3 此或有資產或負債所產生之收益及費用的認列與衡量基礎。

1 請參閱 International Accounting Standard (IAS32), Financial Instruments: Disclosure

and Presentation。